In today’s saturated credit card market, the phrase “best fintech credit card” floats around like a banner with no real anchor. Everyone claims to be the best. But for those of us working at the intersection of UX, payments, and loyalty program analytics, we know better: the right fintech credit card isn’t just a payment tool — it’s a user journey.

If you’re a product manager, CX strategist, or someone responsible for choosing business credit cards, this article will help you cut through the noise. We’ll look at how modern fintech card issuers differentiate themselves, what makes them succeed (or fail) in user experience terms, and how to align credit card issuing with real business needs.

In this list, we present the best fintech credit card 2025 options — selected based on popularity, UX strength, and relevance to modern card issuing needs. Each choice reflects a shift in how financial institutions, startups, and growing businesses approach card issuing services.

1. Ramp – Best for Expense Automation in Fintech Business

Why it’s popular:

Ramp – one of the major credit cards – stands out in the card issuing space by combining finance automation with no annual fees. It’s not just a corporate card, it’s a full-stack card program that reduces manual work. Cards can automatically flag duplicate spend, track vendor usage, and generate insights.

- Tailored for corporate credit cards

- Real-time insights via a sleek online platform

- Great for finance teams in growing fintech businesses

2. Brex – Best for Startups and Small Businesses with No Credit History

Why it’s popular:

Brex has transformed credit card issuing by dropping traditional credit score checks. It calculates limits based on cash flow and allows small businesses to issue virtual cards instantly.

- Flexible card creation and user roles

- Powerful mobile app and analytics

- Favoured by fast-scaling fintech companies

3. Jeeves – Best Cross-Border Fintech Credit Card

Why it’s popular:

Jeeves caters to global teams. It supports multi-currency transactions and offers fast issue virtual cards capabilities — ideal for companies operating across LATAM, US, Canada, and the UK.

- Embedded FX savings for digital payments

- No personal guarantee needed

- Streamlined corporate credit solutions

4. Stripe Corporate Card – Best for Platforms and Developers

Why it’s popular:

Built into the Stripe ecosystem, this credit card issuer provides a seamless connection between your payment card infrastructure and everyday business spend.

- Easy onboarding for Stripe users

- Simple card issuing platform that provides control and rewards

- Great for integrating credit products into workflows

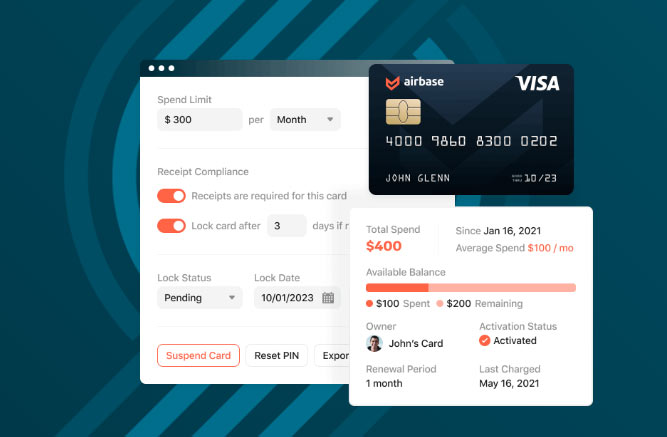

5. Airbase – Best for Financial Control and Prepaid Card Management

Why it’s popular:

Airbase is a go-to for companies needing control across debit or credit cards. It supports prepaid card transactions, spend policies, approvals, and tight control — all through one unified system.

- Strong card issuing solutions and spend visibility

- Useful for managing multiple teams and budgets

- Trusted by CFOs in mid-sized fintech businesses

6. Divvy – Best Free-to-Use Card for SMBs

Why it’s popular:

Divvy’s freemium model and robust budgeting tools have made it a top choice among business card seekers in 2025. You can issue multiple cards, assign limits, and track every penny.

- Appeals to credit builder programs

- Well-rated UX in customer satisfaction surveys

- A rising player among credit card companies

7. Mercury IO Card – Best for Tech Startups

Why it’s popular:

Mercury’s card program integrates banking, treasury, and card issuing. Startups love it for its no-nonsense design, automation features, and instant credit card issuing.

- Transparent fees, sleek UI

- Built for modern fintech business teams

- Enables cards for employees with real-time control

8. Capital on Tap – Best UK-Based Fintech Credit Card for SMEs

Why it’s popular:

This UK-based fintech offers corporate credit cards with cashback, flexible credit limits, and simple onboarding. It’s particularly strong for sole traders and limited companies.

- Strong credit card products for UK businesses

- Rewards transparency and account flexibility

- Fast card issuing services with high satisfaction

9. Nav Business Card Finder – Best for Credit Score Matching

Why it’s popular:

Nav is not a card issuer, but its tool matches your business profile to available credit card options, including secure credit card or charge cards. Its popularity lies in guidance.

- Perfect for exploring top 10 credit card options

- Supports businesses with poor or thin credit history

- Empowers better decisions through personalized filters

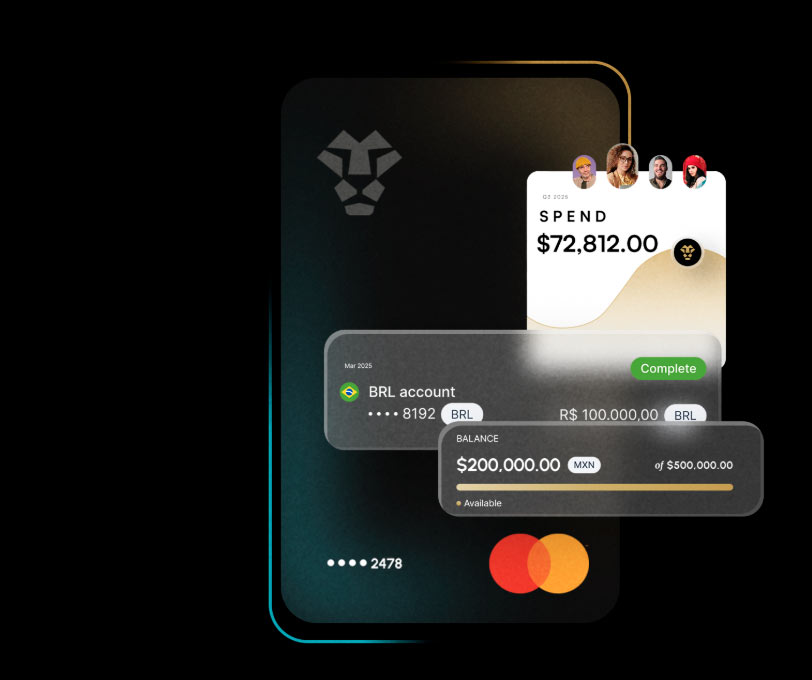

10. Revolut Business – Best Fintech Card for International Teams

Why it’s popular:

Revolut Business has emerged as a powerful player in global fintech card management. It supports virtual and physical cards, currency exchange, and custom permissions.

- Designed for global fintech companies

- Ideal for prepaid card issuing and borderless finance

- Smart controls with a mobile-first approach

Fintech Credit Cards: Not Just a Sleek App

Fintech credit cards often come wrapped in the glow of innovation: real-time dashboards, instant card issuance, sleek mobile apps. But the UX research says otherwise — many users still abandon card apps because of clunky onboarding, unclear credit limits, or poorly communicated card management policies.

Here’s the truth: a good fintech credit card doesn’t just digitise old systems. It redesigns them.

Let’s take Ramp, Brex, and Jeeves — some of the top fintech players in this space. All offer virtual and physical cards, fast approvals, and spending controls. But what sets them apart is how they approach card issuance as a product, not a utility.

For example:

- Ramp automatically categorises spend data and nudges employees to save. That’s not just helpful — it’s behaviourally smart.

- Brex offers multiple cards with tailored credit limits based on real-time cash flow, not outdated credit checks.

- Jeeves, especially for global startups, simplifies cross-border card issuing without requiring multiple local banking relationships.

These aren’t just features. They’re examples of user-centric design solving real pain points in the fintech industry.

What Makes a Fintech Credit Card the “Best”?

Here’s our framework at FinUXlab for evaluating the best fintech credit card:

1. Onboarding That Builds Confidence

Can users apply without friction? Is the approval process transparent? Traditional credit card companies often bury terms in legalese. Fintech leaders simplify choices using just-in-time guidance — think UI microcopy, visual flows, and tiered explanations of risk and reward.

2. Control, Not Complexity

Cards for employees should be easy to issue — and just as easy to revoke. The best card issuing platforms offer real-time card management, permission levels, and category restrictions built into the mobile app.

This helps businesses avoid budget leaks and gives users psychological ownership — one of the key UX principles in financial design.

3. Flexible Credit Limits Based on Context

Why penalise a startup founder with no formal credit history? The best card issuing models (like those from UK-based fintech providers) assess revenue, platform integrations, and banking activity — not just FICO scores. This allows for adaptive credit lines that evolve with a business, not against it.

4. Transparent Rewards That Don’t Disappear

Too often, business credit cards tie loyalty to opaque systems. Points expire. Categories rotate. Users feel trapped.

Fintech cards that succeed — like those linked to Stripe, Mercury, or Wise — offer cash-back, fixed-rate returns, or even crypto rewards. And more importantly, they show your earnings clearly inside the app. No more digging through PDFs to understand what your cards offer.

Traditional Cards vs. Fintech Cards: What the UX Research Shows

We’ve run diary studies and quant surveys comparing experiences between traditional credit cards and fintech-issued ones. Here’s what we learned:

| UX Factor | Traditional Cards | Fintech Cards |

|---|---|---|

| Onboarding Time | 3–7 days (avg.) | Under 10 minutes |

| Clarity of Credit Terms | Often vague | Contextual and adaptive |

| Employee Card Management | Manual and rigid | Dynamic and app-based |

| Rewards Transparency | Poor | Real-time feedback |

| Customer Service Touchpoints | Phone/email only | In-app, live chat, self-serve |

These differences don’t just improve satisfaction — they reduce churn, especially among small businesses and high-growth startups who need cards that can be used instantly and adjusted on the fly.

Who Is the Best Card Issuer for Your Use Case?

The answer depends on your specific business goals. Here’s a quick UX-informed guide:

| If you’re… | Look for a card that… |

|---|---|

| A fast-scaling startup | Offers dynamic limits and multi-currency support |

| A small creative agency | Provides virtual cards and category-based spend controls |

| A marketplace operator | Supports prepaid or debit card issuing for sellers |

| A global team leader | Enables borderless card issuing services and FX savings |

| A credit-builder SME | Links to revenue-based credit builder paths |

Why UX Still Defines the Winner in Card Issuance

The card industry is evolving fast. But as card networks, open APIs, and embedded finance blur the lines between debit and credit cards, the defining success factor isn’t technological firepower — it’s user clarity and trust.

In this environment, credit card companies and payment networks are no longer just back-end facilitators. They are part of a visible user journey. The experience a business has when managing limits, issuing cards to employees, or navigating terms is just as important as the underlying card processing companies or cc vendors behind the scenes.

Many businesses know what the 4 major credit cards are — Visa, Mastercard, American Express, and Discover — but few understand how the UX surrounding these brands determines loyalty. The big 4 credit cards each sit atop a complex payment processing network, yet users don’t interact with the network — they interact with the experience that frames it.

And that experience is often inconsistent. A major credit card might offer competitive rewards but provide a clunky portal for adjusting limits or understanding charges. Meanwhile, a nimble best fintech credit card might not have the brand recognition of the largest credit card processors, but wins with seamless onboarding, instant spend controls, and transparent logic behind credit decisions.

In short: technical capability has become commoditized. UX has not.

Whether you’re evaluating a list of credit card networks, comparing the market share of Visa against alternative to Mastercard and Visa providers, or assessing major payment processors, the differentiator isn’t found in a list of major credit cards or a list of debit card networks — it’s in how easy they make it to issue, understand, and use the product.

Consider this: the best credit card payment system is one your users don’t have to think about. They know how to use it, what it costs, and what they’re getting. That level of confidence only comes when credit card providers and card issuers treat UX as a strategic priority — not a post-launch patch.

From mypayment insider platforms to legacy visa competitors, everyone is vying for relevance. But only those who embed clarity, empathy, and accessibility into their payment card flows will earn long-term trust.

UX isn’t a wrapper around the best card issuing tech. It is the tech — the part users experience, remember, and return to.

Final Thoughts from the FinUXlab Team

FinUXlab Expert Comment:

Choosing a card today is a bit like online dating — endless profiles, shiny features, and the lingering question: is this one really right for me?

Many credit card options promise love at first swipe, but without clarity, they end in ghosting. Sure, credit cards offer cashback, points, even crypto — but what happens when you try to adjust credit limits, or assign spending roles across teams? That’s where the romance fades.

Fintech cards often charm with design, but not all follow through on substance. And while credit cards also boast innovation, too many card issuing companies still deliver experiences that feel like 2009 wrapped in a 2025 pitch deck.

At FinUXlab, we help you figure out which card is right — not just on paper, but in practice. Whether you’re exploring a range of credit card products, planning to launch your own fintech credit cards offer, or just trying to make sense of what cards often provide, our experts translate complexity into clarity.

Because even the friendliest credit union UX won’t save you if the friction’s baked into the flow. Let’s make sure your users never have to swipe twice to understand their card.

As researchers and consultants in financial UX, we’ve seen time and again how the “best” card on paper can become the worst in practice if the design fails to meet user expectations.

So before selecting from the top 10 credit card options or launching your own card issuing platform, ask the real questions:

- Will your users understand their limits and rewards at a glance?

- Can they fix errors or freeze a physical card without calling support?

- Do they feel in control — or locked in?

If you’re unsure how your product measures up, we invite you to join one of our fintech UX seminars or book a diagnostic session.

Because in the end, the best credit card is the one users don’t have to think about.

Let us help you get there.